Trade tariff policy and inflation continue to drive market volatility. Capital markets have experienced some of the most volatility in recent memory due to the draconian tariff policies announced by the Trump Administration on April 2nd. As April 2nd approached, markets were optimistic that the announcement would be measured, as evidenced by the DOW above 42,000 and the 10-year Treasury Bond yield at 4.2%. Then on April 2nd, the Trump Administration announced its global tariff policy, stated to be “reciprocal”. In my opinion, the tariff calculations were ill-founded and the announcement irresponsible. The tariff percentages were not based on other countries’ tariffs but rather on a bizarre calculation of a country’s surplus and exports. It is my hope that the tariff schedule announced on April 2nd has found its way to the shredder.

These tariffs injected fear into markets like the legendary Sword of Damocles. The DOW declined 4,500 points, and the 10-year treasury yield rose from 4.2% to 4.5% in the five trading days following April 2nd.. Then, on April 9th, the Trump Administration put a 90-day pause on the April 2nd tariff announcement, and markets firmed up with the DOW rallying to 40,642 by the end of April and the 10-Year Treasury Bond yield declining to 4.2% as buyers came back to these two important US markets.

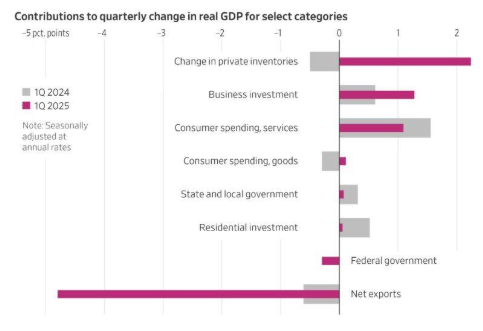

The Bureau of Economic Analysis (BEA) announced on April 30, 2025, that the US economy contracted by -0.3% as measured by Gross Domestic Product (GDP). The chart to the right (source: Wall Street Journal) shows consumer spending and business investment growing solidly, and not surprisingly, a contraction of federal government spending. Inventory builds and imports were high due to tariff policy, with inventory building being a plus and imports being negative to the GDP calculation. The stock market sold off swiftly when the headline broke, only to recover as investors were less worried when assessing the various GDP components. These data are all pre-April 2nd; therefore, market anxiety persisted because the real potential economic concerns would be post-April 2nd.

The stock market rebound during the past 10 days is encouraging, with the Dow Jones Industrial Average rising more than 3,000 points. The April jobs report was released on Friday, May 1st, with a 177,000 increase in payrolls for April, giving investors optimism along with the Trump Administration moderating its tariff rhetoric.

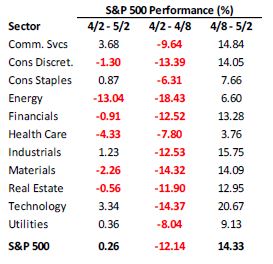

Markets move rapidly, making “timing the market” increasingly difficult. We advise against attempting to do so. We continue to advise clients to invest in equity markets with a time horizon of three years or more. When one attempts to time the market, one needs to make two prescient decisions: when to sell and when to buy back into the market. The table to the right (source: Bespoke Capital Research) illustrates the speed and amplitude of the recent market behavior.

Markets remain uncertain regarding tariff and tax policies. The Trump Administration states it is in active negotiations with most of its largest trading partners. Markets are waiting for “deals” to be announced, which will help ease investor uncertainty, in my opinion. If these negotiations drag out into the second half of 2025, a recession could unfold. Businesses need policy clarity to make capital decisions. If “deals’ begin to be announced by the end of June, markets may exhibit optimism.

Tax policy uncertainty is weighing on markets as well. Many provisions of the Tax and Jobs Act of 2017 (TCJA) will expire at the end of 2025 unless Congress extends or makes permanent TCJA. If tax rates and key provisions (child tax credit and 20% deduction for business pass-through income) revert to pre-TCJA, consumer and business demand would likely be constrained and push the US economy into contraction (recession). I expect Congress to pass legislation to resolve this tax policy uncertainty, and I hope for legislation to be signed by June 2025. This would give markets a well-needed dose of optimism as well.

Where do we go from here? The market appears to be primarily, if not myopically, focused on tariff policy. The stock market rebounded 8% from its recent low on April 21st as tariff rhetoric eased, and possible negotiations with China may be in the offing. Markets are waiting for “deals” to be announced, the sooner the better. Agreements with Japan, Korea, and India may be the first group of countries with which agreements may be announced. The Trump Administration’s tariff policy goal is to motivate our trading partners to significantly reduce tariffs and other non-monetary trade restrictions. We do not expect a zero-tariff world in six months. However, if negotiations result in agreements to substantially reduce these trade barriers in 3-4 years, I believe markets will respond positively. My reasoning is quite simple. Other countries impose trade restrictions on U.S. imports to protect particular industries and to raise revenue to support their governments’ spending. A 3-year guide path gives these countries time to restructure their revenue and expense budgets. At the same time, businesses will have policy clarity to make capital investment decisions to expand capacity in the U.S. if they see economic opportunities to exploit. Modern-day factories include highly automated systems that take time to build. A 3-year window may be ideal. Most countries are feeling economic pain due to the tariff war. And because of this shared pain, I believe countries will negotiate and agree to a trade settlement, as it is to all countries’ benefit.

IF NO TARIFF DEALS ARE ANNOUNCED,

ALL BETS ARE OFF AND A RECESSION MAY UNFOLD.

While progress on the tariff front is necessary to move markets higher, the passage of legislation to affirm the current tax structure and the commencement of reducing interest rates by the FED during the second half of 2025 should provide tailwinds as well.

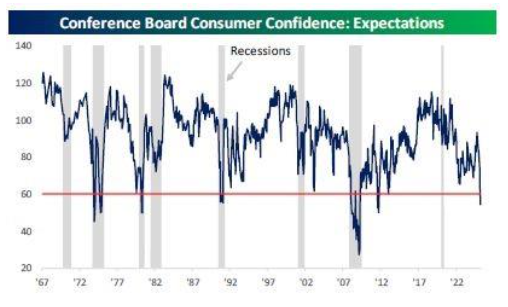

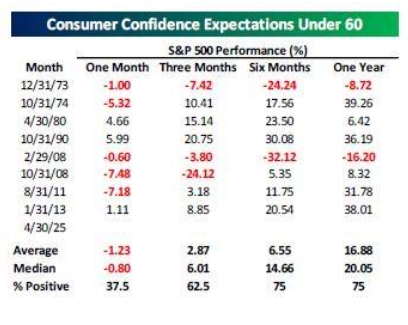

Consumer Confidence is in the tank! However, don’t fret- as the musician Bobby McFerrin wrote in 1988, “Be Happy Don’t worry.” Consumer sentiment tends to be a contrarian indicator to the stock market.

As the above chart shows, the Conference Board’s Consumer Confidence Index is below 60, and considered extremely bearish. However, look at the S&P Index performance as the following table illustrates. Markets may remain negative for the short term, but when one looks out 6 and 12 months, the stock market is usually higher, with two exceptions: 1973, the Iranian oil embargo, and 2008, the financial crisis.

Rich Lawrence, CFA May 6, 2025

DISCLOSURE:

Opinions about the future are not predictions, guarantees, or forecasts. Investing in stock and bond markets has risks that could lead to investors losing money. We recommend that investors invest in the stock market with a time horizon of three years or more.