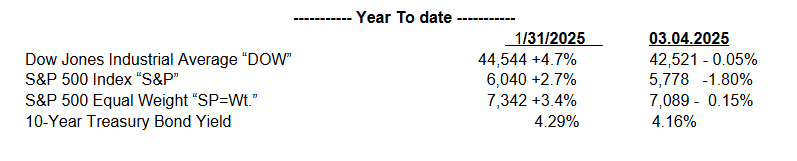

2025 started with a strong January after a 14% gain in 2024, only to give up most of 2025 gains by the beginning of March, as the table below displays. The primary culprit of this recent pullback is the current Trump Administration’s “Administration” tariff policies, which I separate into two categories: 1- the 25% tariff on Canada and Mexico and 20% on China as a policy to motivate these countries to cooperate with the US to reduce the flow of fentanyl into the US; and 2- the “reciprocal” tariff policy set to go into effect on April 2nd. The 25% tariff on Mexico and Canada will cause economic panic to all three countries (Canada, Mexico, and the US). And because of this financial pain, I believe Canada, Mexico, and the US will agree to a cooperative effort, and these tariffs will be removed in the short term. Of course, the leaders of all three countries need to show strength to their respective political constituents and claim “a win”. The uncertainty is causing stocks to sell off.

The reciprocal tariff policy is straightforward: The US will apply the same tariff on the country that places a tariff on US goods and services. The Administration’s goal is for our trading partners to remove trade barriers. If country x has a 15% tariff on US goods, the US will match this tariff. If country x then responds by reducing its tariff to 0, the US will follow and match the – 0 – tariff. The risk is that if countries continue to raise tariffs on each other and they spiral upward, economic growth will be restrained (a possible recession), consumer prices will rise, and the stock market would likely sell off significantly. Alternatively, if trade barriers around the world ratchet down, economic activity among our trading partners would likely expand, giving a boost to stock markets.

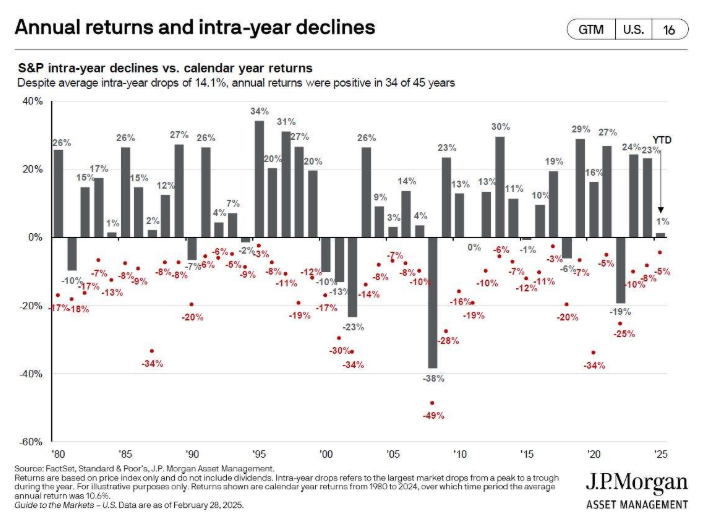

The US stock market declines every year and typically declines by 5-7% from its intra-year high. The following graph illustrates this market behavior. The US stock market has declined 4-5% from its recent 2025 high.

The recent market decline is precisely why we recommend that clients have safety funds (bonds and money market funds) for cash needs for at least 2 years, preferably 3 years.

The driving factors of the stock market remain: the outlook for economic growth, corporate earnings and dividends, inflation and interest rates, and valuation.

U.S. Economic Growth- Economic growth is measured by Gross Domestic Product (GDP) and reported by the U.S. Bureau of Economic Analysis (BEA). GDP is the value of all finished goods and services and is reported with inflation “nominal” and without inflation “real.”. Real GDP measures economic activity. The following estimates illustrate that the U.S. economy is expected to grow and not contract in 2025 and 2026.

Corporate Earnings and Dividends Growth- Above trend for 2025 and 2026- As measured for the S&P 500 Index of companies. The following estimates are from the consensus of securities analysts and strategists.

2025 + 12%

2026 + 14%

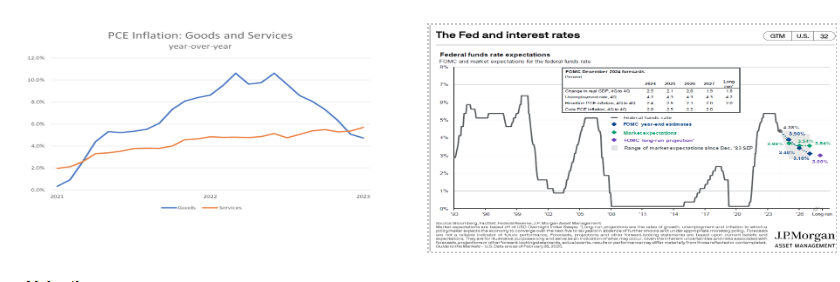

Inflation is declining- slowly; interest rates to follow

Valuation

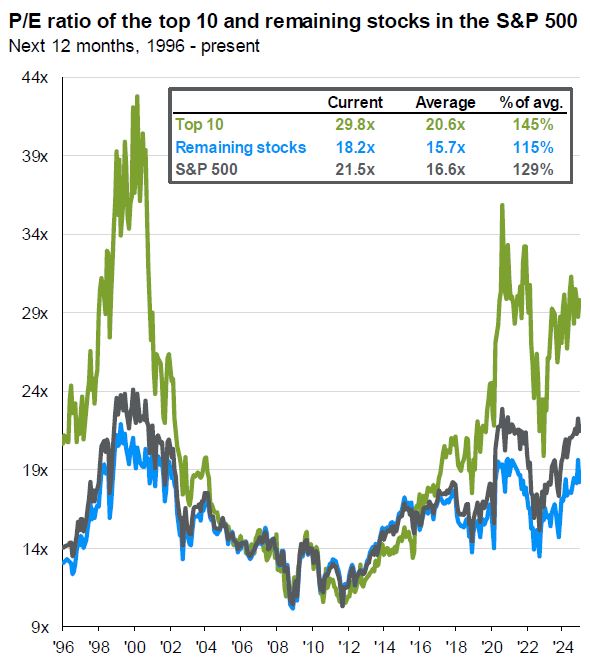

Stocks’ Price-to-Earnings ratio “P/E” is 21.0x and supported by the well-above-average corporate earnings growth estimates for 2025 and 2026 and declining interest rates.

From our February 2025 Client Note

Stock valuations appear high but, in our opinion, are justified by the expected growth in corporate earnings and dividends for 2025 and 2026. The current forward price-to-earnings (P/E) ratio of the S&P 500 “S&P” is 21.9x, well greater than the 16.9x average over the past 30 years. During these 30 years, the S&P earnings have grown 6-8% annually. When considering the S&P 500 companies’ earnings, which are expected to grow 14% in 2025 and 2026, respectively, the above-average P/E is justified, in our opinion. Excluding the largest 10 stocks, the remaining stocks’ P/E is 18.9x, also greater than their 15.8x average. If 2025 and 2026 earnings do not materialize, the stock market will be vulnerable to the downside.

We believe the stock market may experience a 5-10% correction in 2025 due to the likelihood that earnings estimates may be revised downward. For context, the U.S. stock market typically declines by 5-7% during most years. This is not a reason to sell stocks but rather to be prepared for typical volatility and to have the appropriate amount of cash, bonds, and stocks.

Rich Lawrence, CFA March 6, 2025

DISCLOSURE:

Opinions about the future are not predictions, guarantees or forecasts. Investing in stock and bond markets have risks that could lead to investors losing money.