The stock and bond markets are about even from the beginning of 2025 after a higher-than-average, but not unusual, volatility in April. I believe this is a great time to discuss volatility and how to position investment portfolios to achieve capital growth over time while having sufficient funds for short-term needs. To set the framework, volatility is the degree to which an investment declines and rises over time. The three primary investment classes we review are equities/stocks, bonds, and cash; each of which provides important purposes in an investment portfolio and offers differing risks and opportunities.

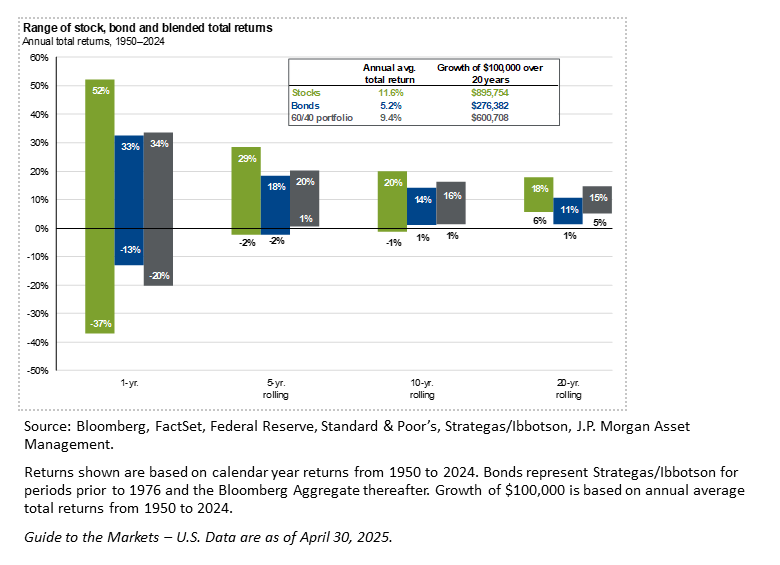

Stocks/equities – As illustrated clearly in the graph on page 4, stocks’ volatility is quite high on a one-year basis (-37% to +52%). This volatility dampens down with time. As the graph shows, on a five-year rolling basis, stocks were down 2% to up 29%. Since 1950 the annualized growth rate of stocks has been 11.6% and since 1980 has been 8.9%. These returns are greater than the 2-3% annual inflation rate which results in wealth and spending power rising for investors capturing these returns.

Bonds- Bonds have both credit and interest rate risk affecting bond prices. Credit risk is the possibility that the issuer (company or government entity) will be unable to pay the contractual interest rate or return the principle amount back to the bond buyer. Interest rate risk is the degree to which a bond’s price rises or falls based on changes in interest rates. When interest rates rise bond prices decline and vice versa. Interest rate risk is higher with bonds with a longer maturity. As an example, if interest rates rise by 1 percentage point, a 10-year US Treasury bond price would decline by 7-8% while a 1-year US Treasury bond price would decline by only 1%. US Treasury yields range from 4% for short term bonds to 4.4% for a 10-year bond. On an after-tax basis these bonds yields provide investors with a return approximately equal to inflation.

Cash/Money Markets- Cash provides safety of principal with very low returns. Cash yields range from 0.2% for bank savings accounts to 4.0% (money markets). Over the long-term inflation eats away at the purchasing power of cash and slowly chips away at one’s wealth. In 10 years, cash purchasing power declines by 25% with a mere 2.5% annual inflation rate.

Investor Dos

- Calculate the amount of cash needed for 3-4 years of spending and allocate these funds to money market funds and investment grade bonds which mature when funds are needed. When investing in corporate bonds, diversify among issuers to no more than 2-4% even with investment grade bonds. There is no financial benefit to concentrate one’s bond holdings with one investment grade bond. Although highly unlikely investment grade bonds can go into default. One needs only to look back to the Enron catastrophe to remember a darling of wall street going bust.

- Take a realistic assessment of one’s tolerance for risk- After computing one’s cash needs from #1 above the result may be a stock/equity allocation of 85%. However, if one is unable emotionally to ride through a steep stock market decline with an 85% allocation to stocks, adjust the stock percentage to a level that one can tolerate during market declines.

- Diversify stock/equity holdings. Unlike investment grade bonds, there is an advantage of concentrating one’s holdings in just a few high growth stocks. However, while stock ownership concentration may lead to outsized returns, this strategy comes with risk. High growth stocks are more volatile than stocks with more moderate earnings potential. Risk and return are aligned. Great wealth is generated with concentrated holdings while a well-diversified stock portfolio protects wealth while participating in the long-term growth potential of the stock market.

- Prepare an Investment Policy Statement- Large institutional investors (pensions, endowments and foundations) prepare an Investment Policy Statement (IPS) which outlines an investor’s:

- Liquidity/cash need

- Risk Tolerance – % in equity, bonds and cash

- Investment time Horizon in # of years

- Special Tax Considerations

- Any special client considerations

The purpose of an IPS is to draft a sound long-term investment strategy designed to achieve investors’ goals. By keeping with a long-term strategy, investors and investment managers follow a set strategy even when markets are volatile. As stated in our IPS which we prepare for clients, the IPS goal is “to follow a sound long-term investment strategy and not to make ad hoc revisions when capital markets exhibit volatility. Volatility may, at times, cause one to respond with euphoria or fear that could precipitate an emotionally based change to your portfolio.”

Investor Don’ts

- Do not chase the hot wall street trend or stock tip. When one attempts to capitalize on a trend, many times it is after the stock or category has had its greatest rise. In other words, don’t chase the “hot stock”!

- Do not attempt to “Time-the-Market”– Market timing in the stock market refers to the strategy of attempting to predict future market movements—such as when to buy or sell stocks—based on expected changes in price. The goal is to buy low and sell high by entering or exiting the market at the most profitable times. The stock market moves very quickly, making it most difficult to make two prescient and timely transactions- to sell before a market downturn, and then to buy at the low point before the market recovers. Many times, the best time to buy is when the financial news headlines are the most concerning and fear-inducing.

Time, Diversification and the Volatility of Returns

Rich Lawrence, CFA June 3, 2025

DISCLOSURE:

Opinions about the future are not predictions, guarantees, or forecasts. Investing in stock and bond markets has risks that could lead to investors losing money.