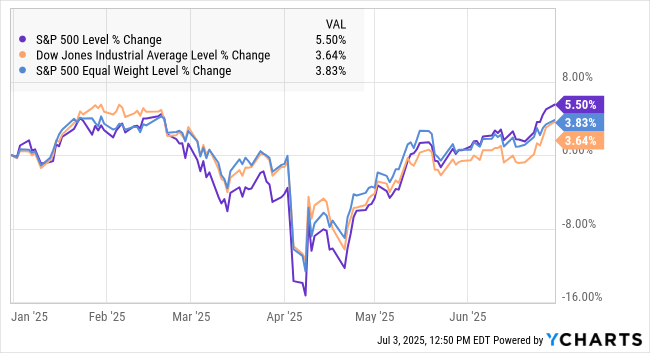

The US stock markets started 2025 with a very strong 10% gain in January, only to correct (decline) by 12% from the start of the year and 16% from its January 2025 high by April 9th. While the stock market is always volatile, this year’s volatility has been 2x the historical average. We attribute this extreme volatility to the Trump Administration’s draconian April 2nd tariff announcement. The stock and bond markets sold off with vengeance, prompting the Administration to place a 90-day pause on the tariff announcement. The pause expires on July 9th. I believe the original tariff announcement will not see the light of day. A 10% base tariff has been implemented to most countries. The goal of the administration is to get our major trading partners to a – 0 – tariff level (including value-added taxes). Considering that our states impose sales taxes of 4-7%, I consider these taxes to be essentially equivalent to the value-added taxes (VAT) imposed by various countries, especially among European Union Countries. So, if the United States and our major trading partners establish a tariff rate (including VATs) at 5-10%, I believe the administration’s tariff policy initiative will be a success.

As we reach the midpoint of 2025, markets are telling a story of resilience amid changing economic, geopolitical, and policy uncertainties. Although headline risks have been numerous—from central bank policy changes to ongoing global tensions—markets have demonstrated an ability to absorb uncertainty, supported by stabilizing inflation, better earnings, and unexpected consumer strength. The proverbial “climbing the wall of worry” should be used to characterize the markets so far in 2025.

U.S. economic growth has slowed but remained positive, with Q2 GDP tracking around 1.7% annualized growth. The long-anticipated “soft landing” scenario seems increasingly plausible. Consumer spending has cooled slightly but is supported by a strong labor market, rising wages, and declining inflation pressures. We continue to believe the Dow Jones Industrial Average “DOW” will be 45,000+ by the end of 2025.

Uncertainty is a fact of investing and always will be. We continue to advise clients to maintain a “safe bucket” of funds, including cash, money market funds, and investment-grade bonds to fund cash needs for at least two years, and preferably 3-4 years. This portfolio structure gives our clients sufficient cash for near-term spending while allocating the balance to equities, which have the potential for capital appreciation well above inflation.

Rich Lawrence, CFA July 5, 2025

DISCLOSURE:

Opinions about the future are not predictions, guarantees, or forecasts. Investing in stock and bond markets has risks that could lead to investors losing money.