2024 was another stellar year for U.S. stock markets; the Dow Jones Industrial Average (DOW) posted a 13% gain, while the technology-heavy S&P 500 Index posted a whopping 23% gain. The Federal Reserve Board (FED) started reducing interest rates in September 2024 once it was confident inflation was on a downward trajectory. The economy expanded, driven by corporate capital expenditures, especially for artificial intelligence “AI”, and consumer and government spending. Together, these factors contributed to the strong stock market in 2024.

Investors open their 2025 calendars with optimism. In 2025, the U.S. economy is expected to expand by 2.0-2.5%, and corporate profits to increase by 14%. The Federal Reserve Open Market Committee “FED” is expected to continue to reduce the Fed Funds Rate in 2025 from the current 4.25-4.50% range to a range of 3.75-4.00% by the end of 2025. Corporate leaders are looking forward to the federal government reducing business regulation and making permanent the current tax structure outlined in the Tax Cuts and Jobs Act of 2017 “TCJA”. Most important is the corporate tax rate of 21%, which was 35% before the passage of TCJA.

Corporate leaders are encouraged that the Trump Administration will implement policy to incentivize investment which should result in continued investment in new technologies. These innovations will likely result in economic growth. An increase in tax revenue, job growth, and productivity will likely flow from capital formation and deployment. The National Federation of Independent Business (NFIB) Small Business Optimism Index rose to 101.7 in November, up from 93.7 in October, surpassing the 50-year average of 98 for the first time in 34 months. This surge in optimism is largely attributed to the recent presidential election, which has led small business owners to anticipate more favorable economic policies. Regardless of one’s political leanings, it has never been a good idea to bet against U.S. capitalism, economy, or capital markets. If I sound like a pro-American investor – I am guilty as charged!

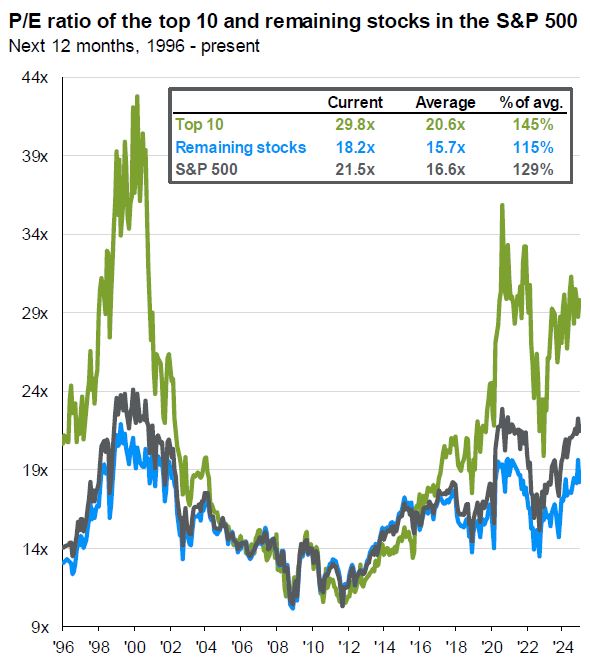

Stock valuations appear high, but, in our opinion, are justified by the expected growth in corporate earnings and dividends for 2025 and 2026. The current forward price-to-earnings “P/E” ratio of the S&P 500 “S&P” is 21.5x, well greater than the 16.9x average over the past 30 years. During these 30 years, the S&P earnings have grown 6% annually. When considering the S&P 500 companies’ earnings are expected to grow 14% and 13% in 2025 and 2026, respectively, the above-average P/E is justified, in our opinion. Excluding the largest 10 stocks, the remaining stocks’ P/E is 18.3x, also greater than their 15.7x average. If 2025 and 2026 earnings growth does not materialize, the stock market will be vulnerable to the downside.

We believe the stock market may experience a 5-10% correction in 2025 due to the likelihood that earnings estimates may be revised downward. This is not a reason to sell stocks but rather to be prepared for typical volatility and to have the appropriate amount of cash, bonds, and stocks.

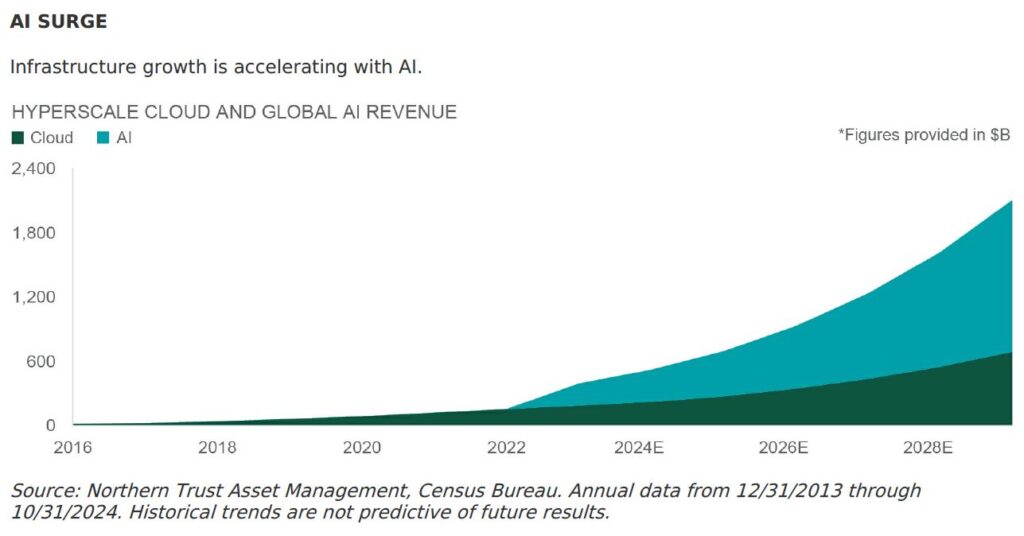

Total Investment (2019-2023): Over the past five years, the U.S. has invested approximately $328.5 billion in AI, with $67.9 billion allocated in 2023 alone, marking a 65.94% increase from 2019. The U.S. invested 35% of global AI investment. (Source: Intelligent CIO).

Market Size Projections: The AI market in the United States is projected to reach $66.21 billion in 2025, with an expected annual growth rate of 27.57%, resulting in a market volume of $223.70 billion by 2030. (Source: Statista).

Revenue Gap Analysis: Some analyses suggest that AI needs to generate an additional $500 billion in annual revenue to be economically viable, indicating a current gap between investment and revenue. (Source: Marketing AI Institute).

The U.S. leads the world in AI development. In 2023, the U.S. developed 63 AI models, well greater than the European Union’s 21 and China’s 15. The world is chasing this new technology, which is expected to transform how business is conducted. (Source: The AI Index 2024 Annual Report by Stanford University).

Implications for Investors

Investment capital flows to new transformative technologies with a vengeance as it has always done. In 1900 there were 2,000 automobile companies in the U.S. many of which were short-lived. The Dot.Com era of the 1990s experienced a similar flow of capital and the subsequent demise of marginal producers. The challenge is to invest in successful companies while limiting losses from companies that end up on the list of failed companies. In doing so, we rely on portfolio managers and research firms to help structure our portfolios which include AI stocks, along with other stocks of well-positioned companies that serve the investment goals of our clients.

2025- What Could Go Wrong In 2025

Tax rates are set to expire at the end of 2025. In 2017 then-President Trump signed the TCJA which includes several tax cuts that have been in place for the past seven years. Investors and corporations are expecting the TCJA tax rates to be extended or made permanent. However, investors are a bit on edge and may remain so, until this legislation is passed.

The TCJA reduced the corporate tax rate from 35% to 21%. Shortly thereafter $1.5 trillion was repatriated back to the U.S., with Apple, Inc. bringing back $500 billion of cash to the U.S.

Deficit spending and federal debt- If Congress and the President make meaningful progress with the deficit, markets will likely respond positively. Conversely, if deficit spending continues at the current level, inflationary concerns and interest rates may rise, causing markets to decline. The time is now for Congress and the President to act and put in place a credible plan to include entitlement program spending constraints.

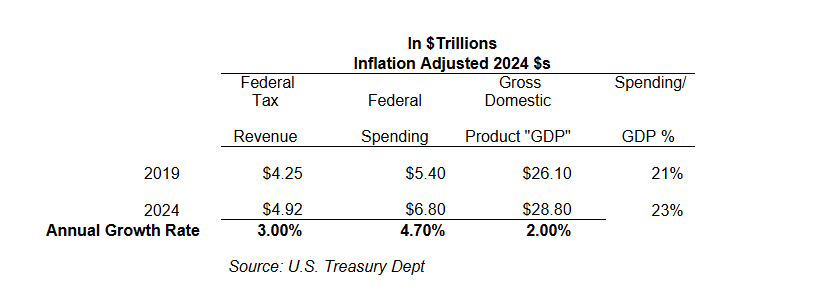

The Federal Government continues to spend beyond its means with a 2024 deficit of $1.8 trillion. In 2024 the federal government spent $6.8 trillion (23% of gross domestic product “GDP”), up from 21% in 2019. The following table illustrates clearly that spending and tax revenue grew faster than GDP; with spending growing 57% faster than tax revenue.

Rich Lawrence, CFA January 6, 2025

DISCLOSURE:

Opinions about the future are not predictions, guarantees or forecasts. Investing in stock and bond markets have risks that could lead to investors losing money.