The stock market came out of the gate in 2025 with strong gains- As of January 31, 2025, on a year-to-date basis:

Markets experienced volatility as usual. In the final months of 2024, the stock market rallied as investors exhibited optimism about a business-friendly environment under the Trump Administration. In December, markets pulled back after the FED signaled it was in no rush to reduce interest rates due to inflation not declining as previously expected. As 2025 unfolds, policy announcements from the Trump Administration are giving investors angst. Just a few Trump Statements- taking over the Panama Canal, Canada being the 51st state, the US owning Gaza and Greenland, and, of course, Tariffs on Canada, Mexico, and China. Markets declined swiftly when the tariff announcements were made, only to rebound when they were delayed for Mexico and Canada. I refer to these comments as “Trump Speak.” I believe markets will look beyond exaggerated statements and assess the actions and policies that will be implemented. I expect more than average stock market volatility due to markets assessing the effects of federal policy changes on the economy, especially when it comes to tax and tariff policy. Markets will respond to the economic effects of policy changes and not to rhetoric, in my opinion. The Trump Administration will not be short with exaggerated rhetoric- yes, Trump Speak.

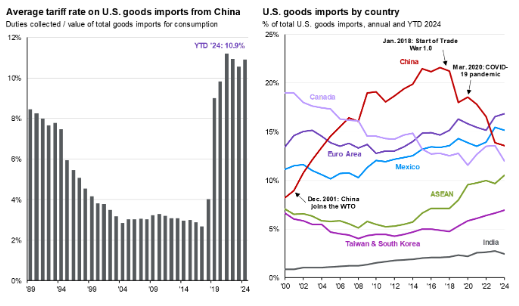

Clients from both political party affiliations have expressed concern about how tariffs may affect our economy and the stock market. The U.S. has a $1.1 trillion trade deficit, with China and the European Union contributing $300 billion and $265 billion, respectively, to the U.S. trade deficit. China captures $300 billion of currency annually, or $3 trillion over ten years, from its trade surplus with the U.S. China allocates these dollars to US Treasury bonds, giving the country a claim on the US taxpayer, to build up its military and to purchase assets across the globe, including in the US. The Trump Administration’s “Administration” trade objective is to bring production back to the U.S., thereby reducing its trade deficit with China. On February 4th, 2025, the Administration imposed a 10% tariff on China imports. China retaliated with 10-15% tariffs on various U.S. imports and imposed regulatory policies to limit U.S. imports. The U.S. imports approximately $450 billion of goods from China, representing less than 2% of the U.S. $28 trillion GDP. If 100% of the tariff cost is passed onto U.S. buyers, the tariff amount would equal a 0.16% price increase to U.S. buyers, assuming no other offsets. As of this writing the Administration’s announced 25% tariffs on Canada and Mexico imports are on pause.

China’s exports to the U.S. as a percentage of all U.S. imports have declined significantly since the COVID-19 pandemic as companies have been shifting supply chains away from China. As the right panel of the graph below shows, US imports from China have declined from approximately 23% to the current 14% of total U.S. imports.

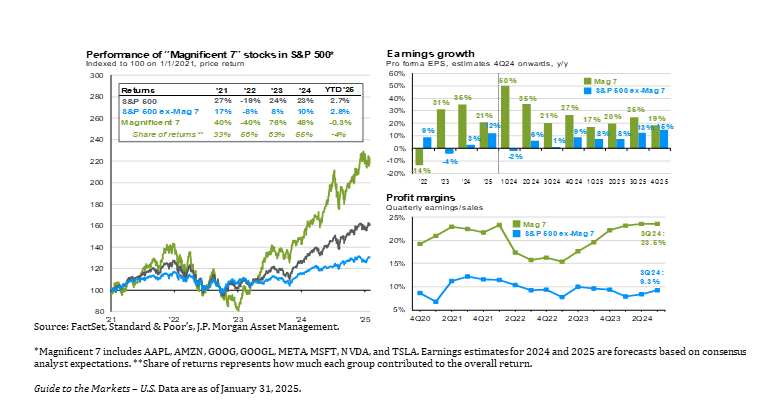

Earnings season is unfolding as I write this commentary, with the majority of companies reporting revenue and earnings better than forecasted. Corporate earnings growth for 2025 and 2026 appears strong at the current time. Investors are expecting earnings for the S&P to grow 14% for 2025 and 2026, well above their 6-8% annual growth rate trend range. Earnings growth may prove to be less robust than expected by the market. Earnings growth during the past two years has been the most prevalent among the largest growth companies (the magnificent seven “Mag-7”) in the S&P. This dynamic is shifting, with the rest of the companies’ earnings growth rate rising and the Mag-7 growth rate declining. This is why broad market indices are outperforming the tech-heavy S&P. For this reason, we position client portfolios to be well diversified to participate in this trend we expect to continue.

The following graphs clearly illustrate the underlying factors of the S&P stock performance and earnings The “Earnings Growth” chart shows the earnings growth improvement of non-mag-7 stocks during the second half of 2025.

Interest rates, Inflation, and Government Spending- Inflation disrupts spending and investment decisions to keep ahead of price increases. Also, it reduces the standard of living when prices rise at rates greater than incomes. The Federal Reserve, “FED,” sets monetary policy to accomplish two primary mandates: to achieve full employment and price stability. Full employment is defined as when the unemployment rate is +/- 4.0% and price stability is defined as when the inflation rate is +/- 2.0%. The unemployment rate is currently 4.1%. The Core- Consumer Price Index “CPI” (excluding food and energy) was up 3.2% year-over-year in December 2024 and up 0.2% on a month-to-month basis. The 3.2% year-over-year rate is well greater than the 2.0% target. However, the 0.2% month-to-month increase is an encouraging signal that the CPI growth rate may resume its decline in the coming months. The Fed uses several inflation indicators and places great weight on the Personal Consumption Expenditure Index “PCE.” The PCE is also well above the Fed’s 2.0% target; in December 2024 the PCE was up 2.6% and higher than the 2.4% reported for November. We believe the FED will be in no rush to reduce interest rates while inflation remains elevated, and employment is currently at “full employment.”

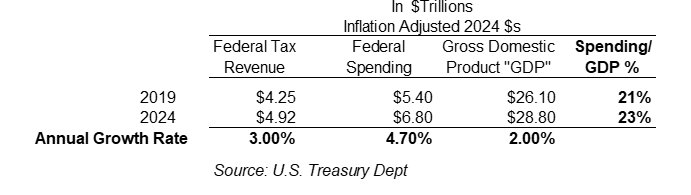

Government spending is one of the main causes of inflation, in my opinion, and needs to be significantly reduced to bring inflation and interest rates down. The well-informed and followed investor Ray Dalio, founder of Bridgewater Associates, discussed this issue in a recent podcast and stated that the U.S. may enter a “debt spiral’ unless our deficit spending is addressed right away. Ray Dalio and Treasury Secretary Scott Bessent both agree that our deficit needs to get to 3.0% of GDP; it is currently 6.8%. The following table illustrates the US has a spending problem:

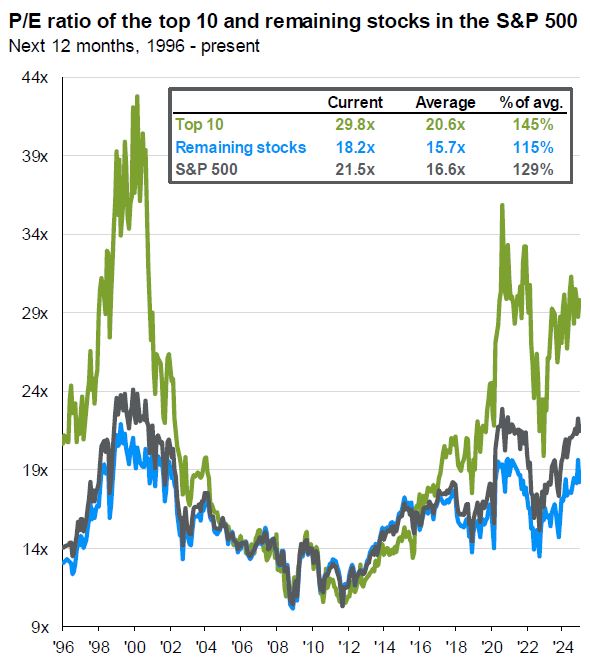

Stock valuations appear high but, in our opinion, are justified by the expected growth in corporate earnings and dividends for 2025 and 2026. The current forward price-to-earnings “P/E” ratio of the S&P 500 “S&P” is 21.9x, well greater than the 16.9x average over the past 30 years. During these 30 years, the S&P earnings have grown 6-8% annually. When considering the S&P 500 companies’ earnings, which are expected to grow 14% in 2025 and 2026, respectively, the above-average P/E is justified, in our opinion. Excluding the largest 10 stocks, the remaining stocks’ P/E is 18.9x, also greater than their 15.8x average. If 2025 and 2026 earnings do not materialize, the stock market will be vulnerable to the downside.

We believe the stock market may experience a 5-10% correction in 2025 due to the likelihood that earnings estimates may be revised downward. For context, the U.S. stock market typically declines by 5-7% during most years. This is not a reason to sell stocks but rather to be prepared for typical volatility and to have the appropriate amount of cash, bonds, and stocks.

Rich Lawrence, CFA February 6, 2025

DISCLOSURE:

Opinions about the future are not predictions, guarantees or forecasts. Investing in stock and bond markets have risks that could lead to investors losing money.