The US Stock Market is up 19% through 11.30.2024, with the large-cap growth index (S&P 500) up a whopping 26%. Economic growth as measured by Gross Domestic Product “GDP” improved during the year and is now expected to be approximately 2.5%, excluding inflation. S&P 500 corporate earnings growth for 2024 is expected to be 9%. The stock market is looking well beyond 2024 and is pricing in corporate earnings growth for 2025 and 2026. Investors are encouraged by the prospect of economic growth policies being promulgated by the new administration in terms of government regulation and tax policy.

Investors were focused on inflation and interest rates in 2024, which I believe will shift to deficit spending and productivity in 2025.

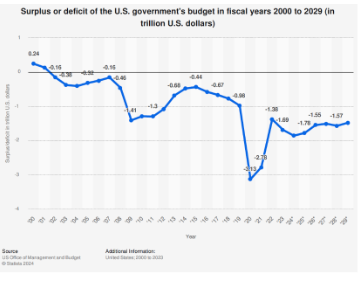

The Federal Government is expected to spend $6.9 trillion in 2024, 9.7% more than it spent in 2023. I believe interest rates will rise for the 3 to 10-year treasury bond unless deficits decline from the current 6.7% of GDP to the low single digits. The recently nominated Treasury Secretary stated a 3% goal by 2028. This would in essence begin the financial deleveraging process by increasing debt at a rate less than economic growth. If a credible plan is put in place, I believe capital markets would reward such a plan.

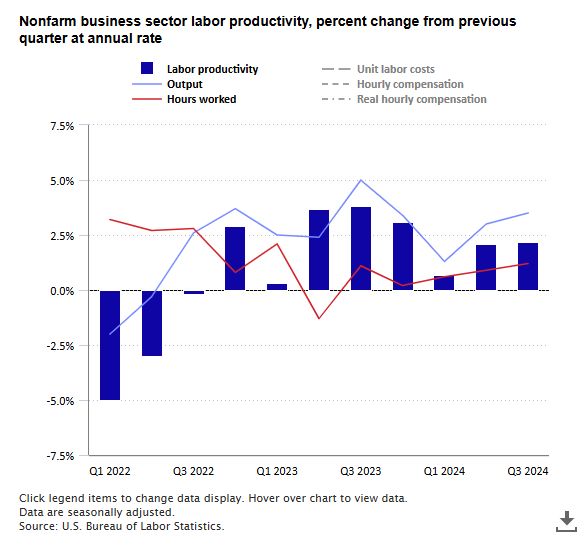

Labor Productivity has far-reaching economic effects in terms of economic growth, income, and standard of living. Labor productivity is defined as the amount of output produced to the amount of labor to produce it. So, if productivity expands the economy expands and employers can increase wages at rates greater than inflation without eroding profitability, truly an ideal situation.

As the chart above illustrates, our economy has been experiencing solid productivity gains driven by capital investment, in general, and especially artificial intelligence “AI”.

The S&P 500 Index is currently priced at a forward price-to-earnings “P/E” ratio of 22x, well greater than the 17x average. The largest 10 stocks of the S&P 500 Index represent 36% of the index. The remaining 494 stocks are priced at a 20x forward P/E ratio (the S&P 500 Index has 504 stocks, not 500). These higher-than-average valuations are due to the higher-than-average earnings growth expectations for 2025 and 2026.

Corporate earnings are expected to rise 24% over the next two years. These estimates are for the S&P 500 Index, which is heavily weighted toward the top seven rapidly growing companies in the index. Excluding these seven companies, earnings are expected to rise by 18-20%. While interest rate policy has a direct effect on the stock market, corporate earnings and dividend growth are essential for stock prices to rise.

2025 Outlook

Positive Tailwinds

- Inflation is heading to the FED’s 2.0% target

- The FED continues to reduce interest rates.

- Earnings of companies in the S&P 500 Index are expected to grow 10-12% in 2025 and 2026

- Federal regulatory and tax policy encouraging economic growth.

Negative Headwinds

- Federal deficit spending continues to put upward pressure on prices by adding to “demand” in the economy, and thus inflation.

- Federal borrowing to fund the deficit “crowds out” the private sector from obtaining necessary capital for private economic growth.

- Geo-political risks – low probability and high consequence of China militarily controlling Taiwan, and thus global semiconductor supply.

- Companies underdeliver earnings growth in 2025 and 2026.

Rich Lawrence, CFA December 4, 2024

DISCLOSURE:

Opinions about the future are not predictions, guarantees or forecasts. Investing in stock and bond markets have risks that could lead to investors losing money.