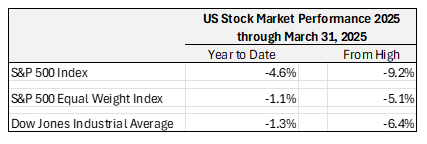

The US stock market started the year with a strong 4-5% gain for the first six weeks, only to give up these gains and some as investors became concerned about consumer spending and tariffs contributing to an already elevated inflationary outlook. When uncertainty rises, markets sell off.

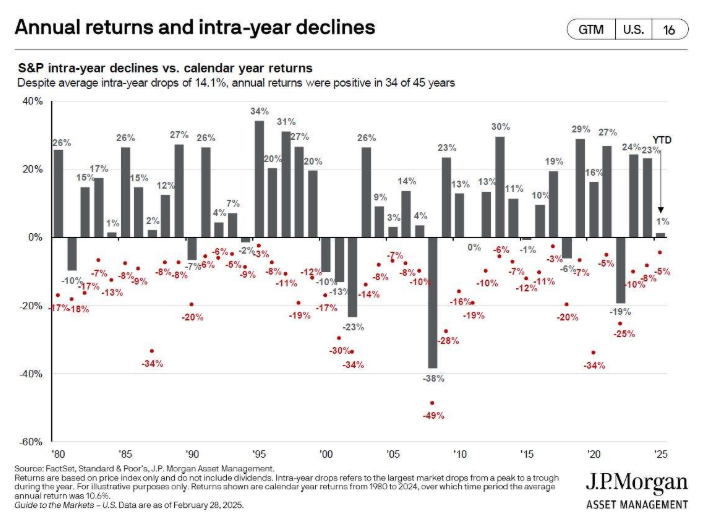

The current stock market sell-off is normal and precisely why we advise clients to have “a safety bucket” (cash, money markets, and bonds) for 3 years or more of spending needs. The following graph illustrates the S&P 500 Index annual returns and intra-year declines.

Our “safety bucket strategy” is based on our understanding that the stock market declines periodically and rises over the long term. When the stock market declines, if one has sufficient safety-cash for spending needs for three years, one does not have to sell stocks when they are down to raise cash for spending needs.

OUR ASSESSMENT OF PROS AND CONS FOR THE MARKET

Pros (Tailwinds)

- While market technicals are weak, market sentiment has gotten way too bearish, in my opinion. The Conference Board, the University of Michigan, and the American Association of Individual Investors surveys all indicate severe pessimism or bearishness. When sentiment gets this pessimistic, it is usually a better time to buy than to bail.

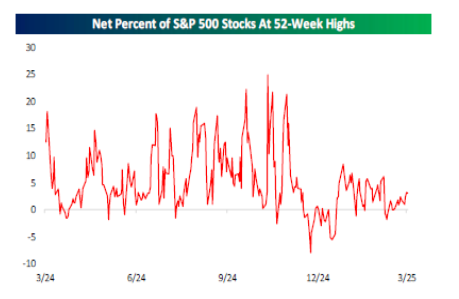

- Market breadth is holding up well. Market breadth is measured by the number of stocks making new highs divided by the number of stocks making new lows. The S&P 500 index price has declined by 5% and 9% on a year-to-date basis and from its intra-year high, respectively. However, the graph to the right illustrates that market breadth has held up quite well.

- The bond market and the FED forecast interest rates to decline in 2025, which is typically a positive catalyst for stocks. The FED is currently on pause and waiting for more evidence that inflation is headed lower to its 2.0% target before reducing interest rates.

- The job market is healthy and balanced, without inflationary pressures. According to the FED’s recent monetary policy statement on 03.19.2025, “….labor market conditions remain solid.”Non-Farm Payrolls Job Growth- 2025

January- 143,000

February- 151,000

March- 150-160,000 (estimate) to be reported April 4th by the Bureau of Labor Statistics “BLS”

The Cons (Headwinds)

- First and foremost- Tariffs! Business leaders and investors are uncertain as to the Trump Administration’s tariff policy to be announced Wednesday, April 2nd. The Administration stated that tariff policy will be ‘reciprocal’ to establish a level playing field with tariffs, including the European Union countries’ value-added tax (ranging 5-14%). We expect this uncertainty to moderate once the Administration announces the tariff schedule on April 2nd.Total US imports of goods and services in 2024 reached $4.1 trillion, or 14% of the Gross Domestic Product (GDP). Goods imports were $3.3 trillion, or 11% of GDP. If one applies a 10% tariff across the board to all goods imports the result would be a one-time price increase of 1.1% if importers can pass along 100% of the tariff price increase. The Administration also stated a 25% tariff on all auto imports but excludes any auto import covered by the United States-Mexico-Canada Agreement (USMCA). The weighted tariff for US imports is 2% versus our trading partners’ 6%. President Trump stated that the new US tariffs would generate $600 billion for the US Treasury. The math does not add up! So, we, along with the market, are waiting with great anticipation for the April 2nd tariff policy announcement.

- Economic growth is slowing– Gross Domestic Product (GDP) estimates for 2025 have declined to the 1.5-2.0% range, down from 2.0-2.5%. Securities analysts and strategists estimate corporate earnings growth for 2025 to be 11.4%, down from their previous estimate of 14.2% in December 2024.

- Several provisions of the Tax Cuts and Jobs Act (TCJA) of 2017 are set to expire at the end of 2025.

- The Trump Administration and the GOP controlled (barely). Congress are currently negotiating details of legislation to make permanent the current tax structure, with a few additions and changes.

- Until this legislation is passed, tax policy uncertainty will continue to haunt the market as well.

- If the current tax rates are not made permanent, taxes would rise substantially and likely push our economy into a recession (economic contraction).

- The median correction since 1952 is -15%. More pain could be in store if the current correction matches history.

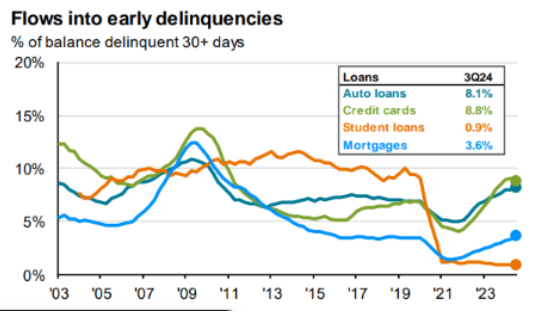

- The consumer is showing signs of stress, as shown by the delinquency graph to the right. The delinquency rates are rising, especially among consumers at the lower income brackets. While the current delinquency rates are on an uptrend, we expect the trend will likely be contained as long as the US job market remains solid.

Rich Lawrence, CFA April 1, 2025

DISCLOSURE:

Opinions about the future are not predictions, guarantees or forecasts. Investing in stock and bond markets have risks that could lead to investors losing money.